The Wholesale Electricity Market

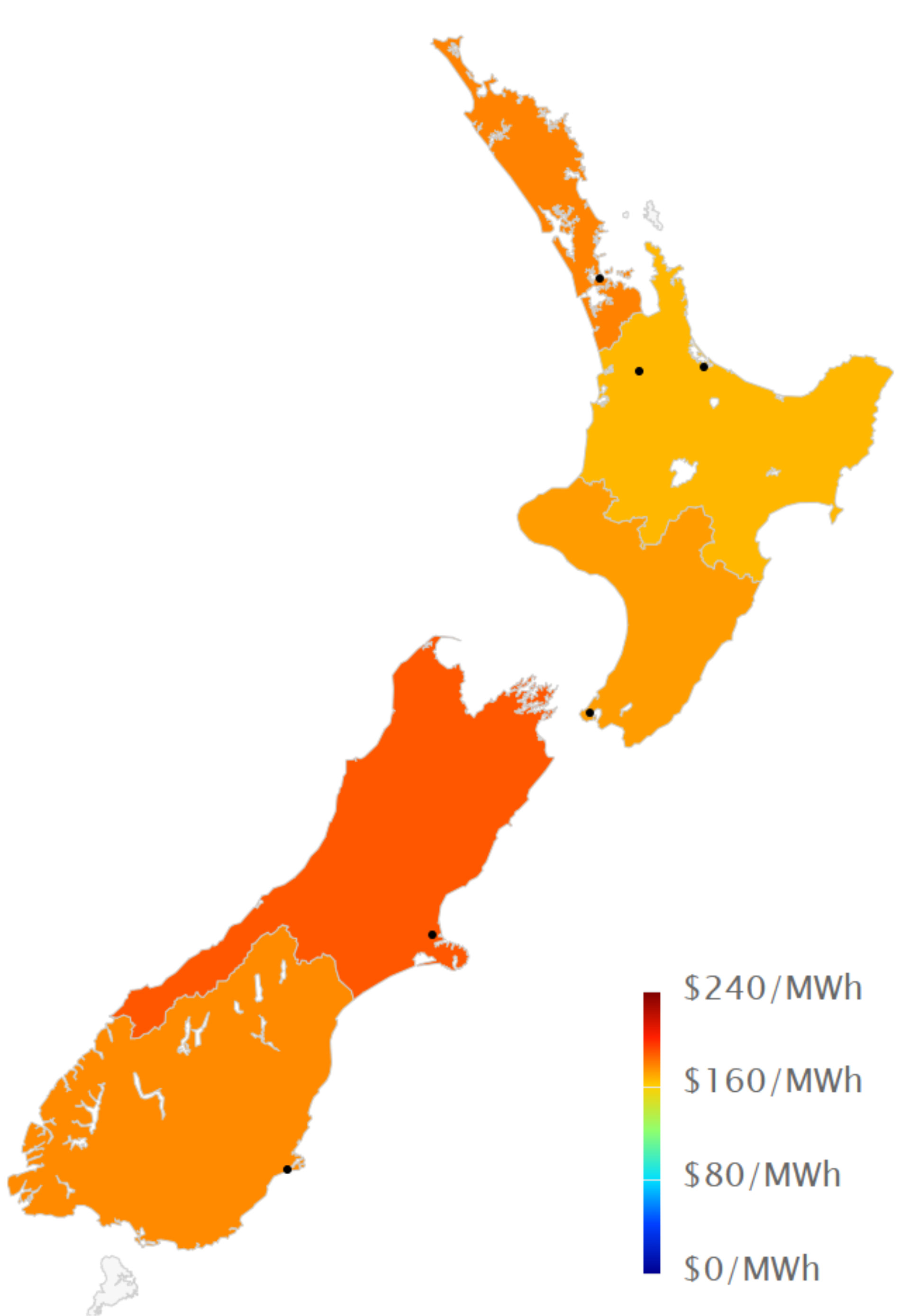

Spot prices in the wholesale electricity market increased significantly during August. Average spot prices for the month ranged from $166 in the central North Island (up from $100 in July), up to $189 in the upper South Island ($108 in July).

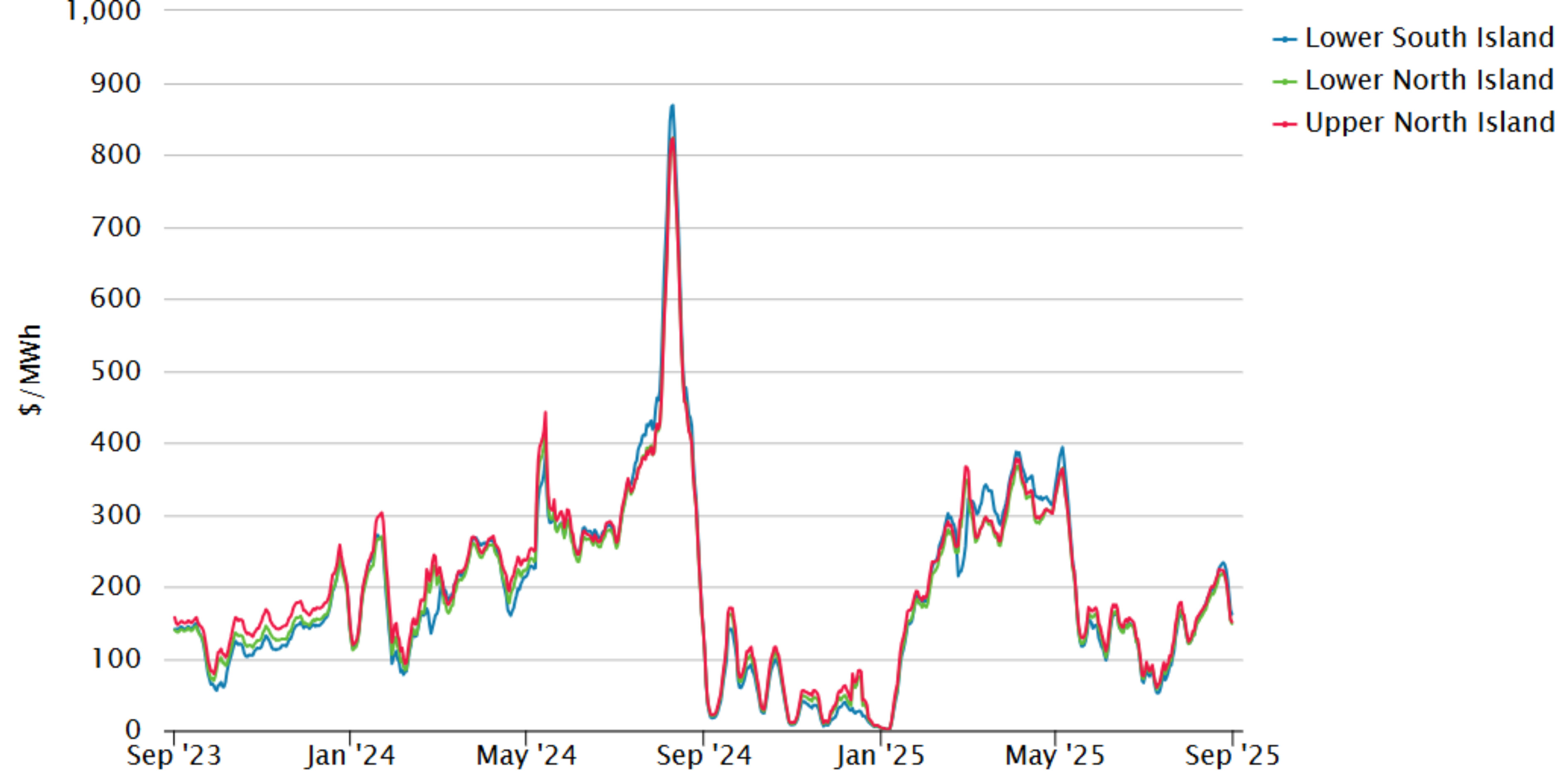

The following chart shows average weekly spot prices over the last 2 years. The recent uptick in prices can be clearly seen.

Electricity Demand

Cold weather through August meant that electricity demand was at the highest levels seen in the last few years as shown below.

Electricity Generation Mix

High demand meant that hydro generation remained at the high levels seen through July, however thermal generation also picked up through August to try to conserve storage.

HVDC Transfer

Power transfers on the HVDC link connecting the North and South Islands are important both in showing relative hydro positions and the reliance on thermal power to meet demand. High northward flow tends to indicate a good SI hydro position, whereas the reverse indicates a heavy reliance on thermal power to make up for hydro shortages.

Northward transfer decreased during August and southward transfer increased to enable SI storage to be conserved.

The Electricity Futures Market

The Futures Market provides an indication of where market participants see the spot market moving in the future. They are based on actual trades between participants looking to hedge their positions (as both buyers and sellers) into the future against potential spot market volatility. They are also a useful proxy for the direction of retail contracts.

The following graph shows Futures pricing for CY 2025, 2026, 2027 and 2028 at Otahuhu (Auckland) for the last 2 years.

Note that $100/MWh equates to 10c/kWh.

Forward prices were up for all years through August. CAL 2026 increased to $222 before falling and ending the month at $203/MWh – up 3% over the month. CY 2027 price was up 4% at $184 while CY 2028 also increased 2% at $178.

Known new generation projects are shown below (additions / removals / changes highlighted in bold).

Hydro Storage

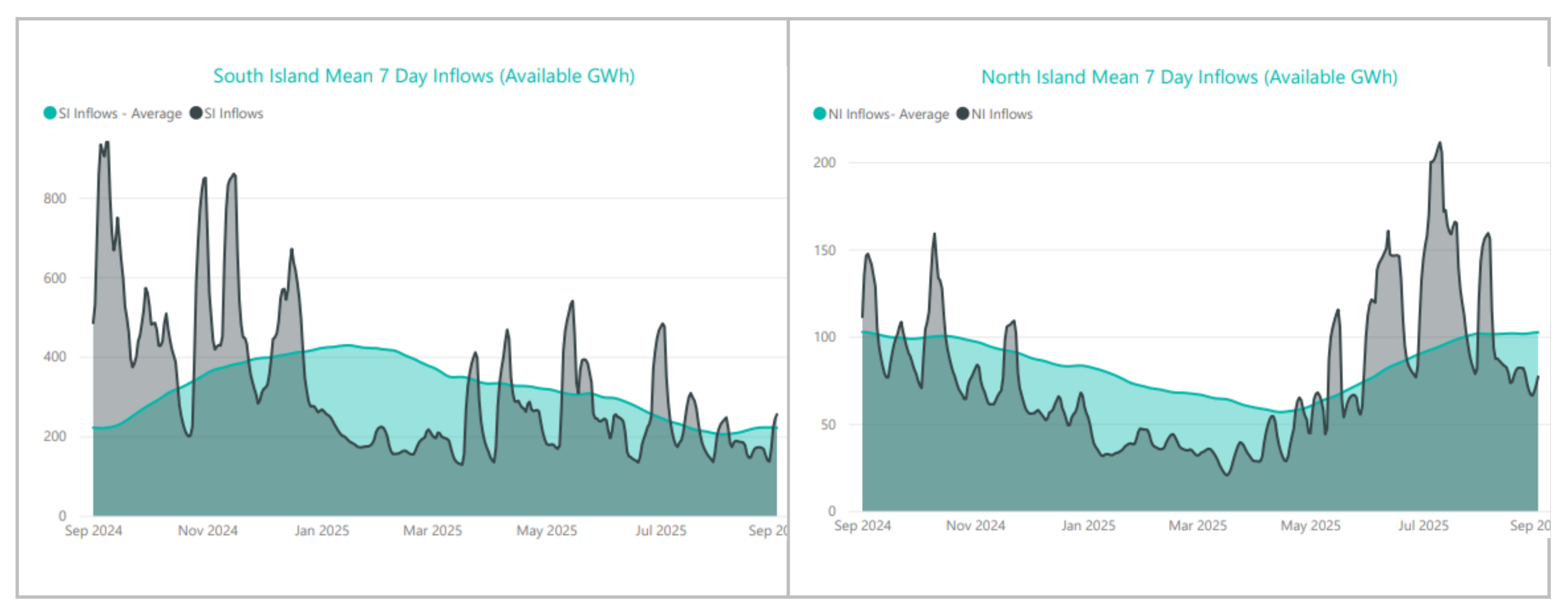

Inflows were well below average in both islands last month as shown below.

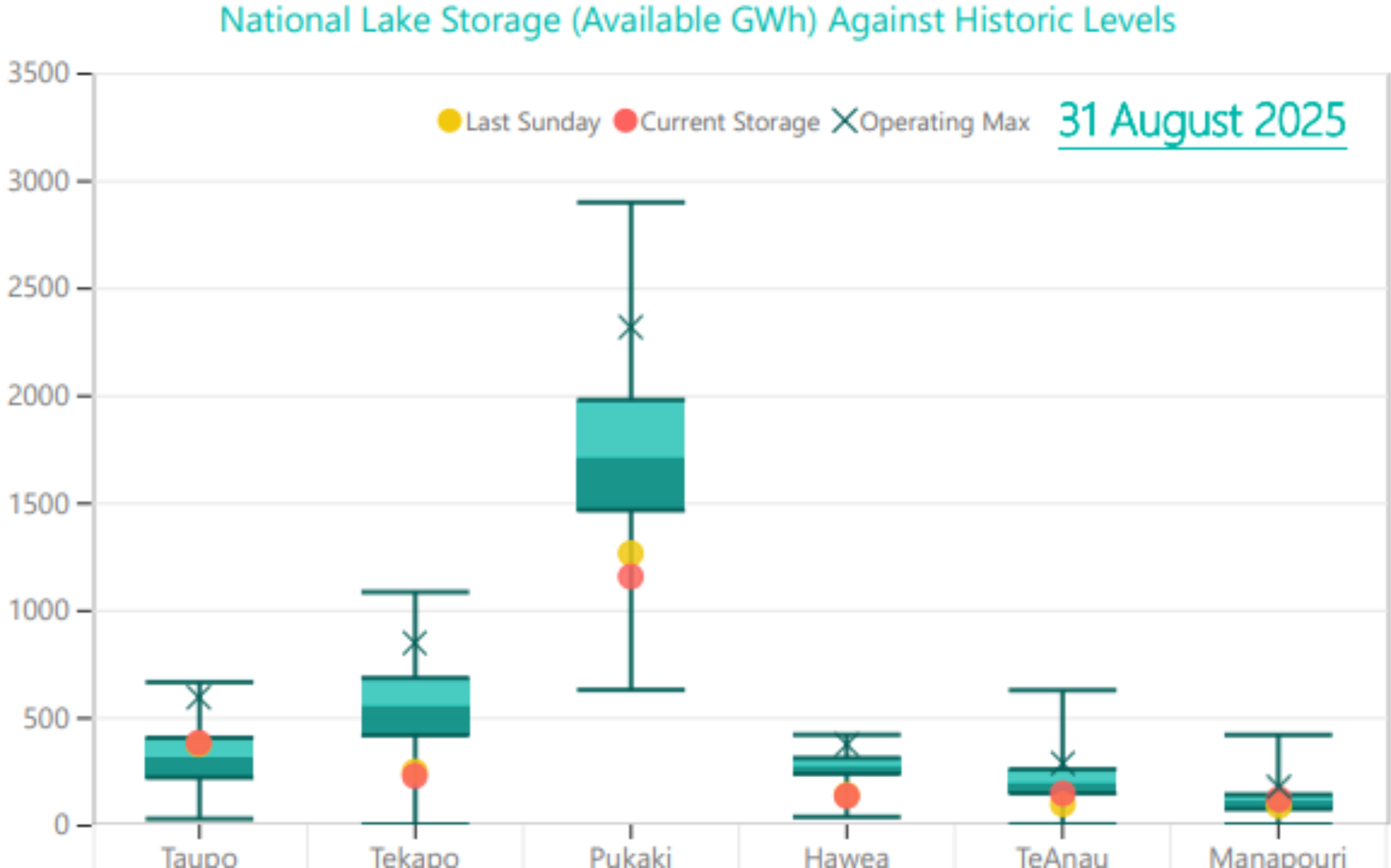

The low inflows and sustained hydro generation resulted in storage dropping rapidly through August. Energy storage levels decreased 681GWh through the month to end at 2,050GWh (45% full). Storage is now well below the average level seen at this time of year. The following chart shows the latest breakdown of storage across the main hydro catchments.

Security of supply risks increased through August with storage levels decreasing as shown below.

Snowpack

Snowpack is an important way that hydro energy is stored over the winter months and released as hydro inflows in the spring. The following graph shows that the snowpack in the important Waitaki catchment increased only slightly during August and is now near the minimum level seen in the last 30 years for this time of year.

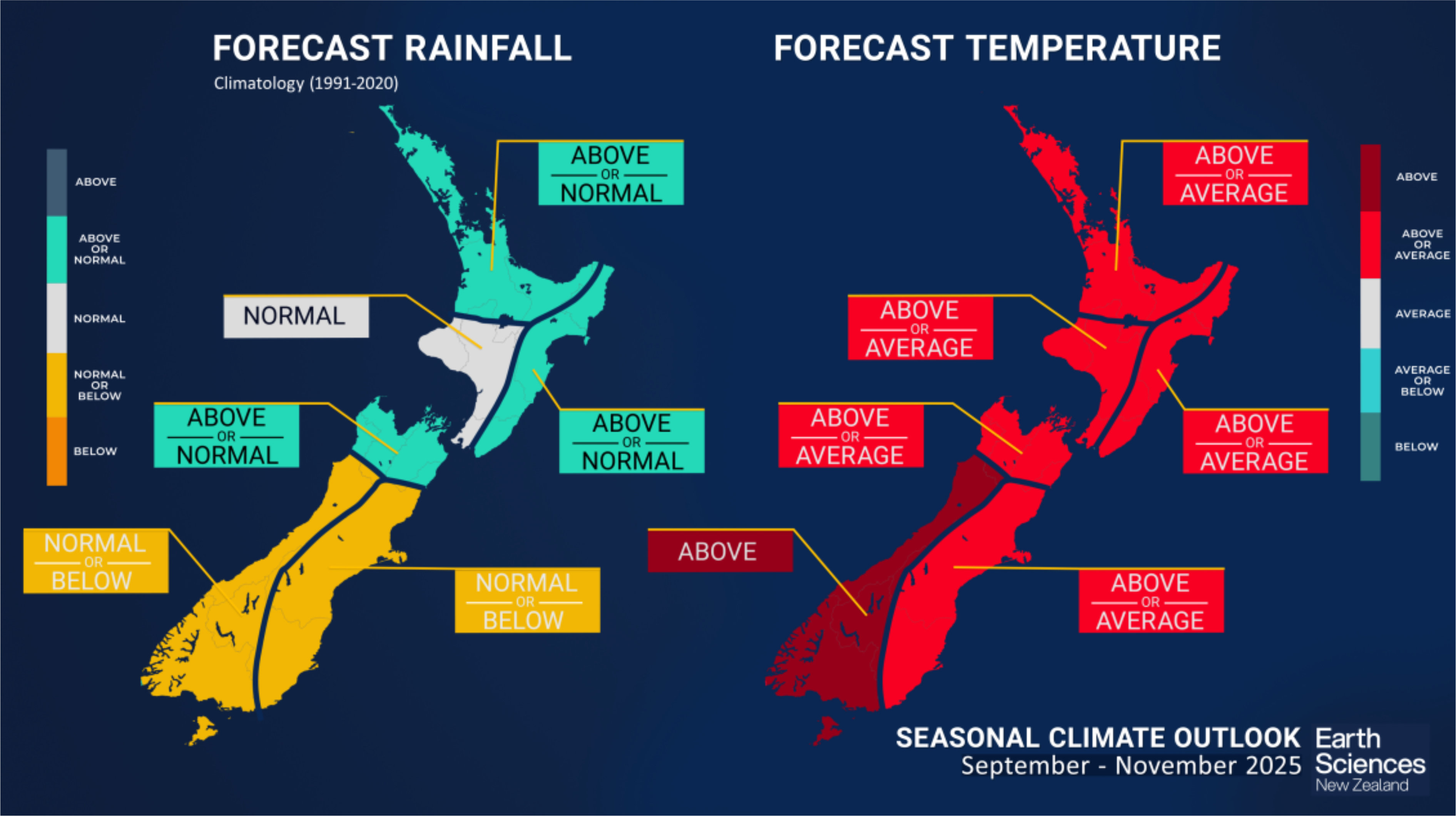

Climate outlook overview July – September 2025 (from NIWA)

- ENSO-neutral (El Niño – Southern Oscillation) conditions remain present in the tropical Pacific, but La Niña-like patterns became more established in August 2025.

- While remaining in the neutral range, sea surface temperature (SST) anomalies in most of the key ENSO regions became more negative during August 2025.

- Subsurface ocean cooling continued in August, with cooler-than-average waters moving eastward and rising closer to the surface in the eastern Pacific Ocean, reinforcing the shift toward La Niña-like conditions.

- International guidance suggests La Niña conditions are favoured during the spring and early summer 2025-26, before returning to neutral. This is further supported by experimental forecasts developed by Earth Sciences New Zealand for the Relative Oceanic Niño Index (RONI), which accounts for the broader warming trend across the tropical Pacific, and indicates that La Niña conditions are likely (60% chance) to emerge over the September-November 2025 period.

- For New Zealand, a westerly-dominated September is expected to transition into a pattern of higher-than-normal pressure over or south and east of the country in October and November. This scenario will lead to alternating periods of settled weather and northeasterly flow anomalies.

- Seasonal air temperatures for the next three-month period are about equally likely to be near average or above average for all regions of New Zealand, except for the west of the South Island, where above average temperatures are most likely.

- September – November rainfall totals are expected to be near normal or above normal for the north and east of the North Island and the north of the South Island. Near normal rainfall is forecast for the west of the North Island. Near normal or below normal rainfall is forecast for the west and east of the South Island. Sub-seasonal, or monthly, projections of rainfall and dryness are updated daily through the NIWA35 forecast.

- During September – November 2025, soil moisture levels and river flows are forecast to be below normal or near normal for the north and east of the North Island and the west of the South Island, with near normal soil moisture levels and river flows expected in the remaining regions of New Zealand.

- Below average hydro storage would persist under the scenario of a drier-than-normal spring for much of the South Island. Currently, many sites that report total storage, river flows, and snow cover are below typical levels for this time of year.

- SSTs remain above average off the west coasts of both the North and South Islands and anomalies intensified slightly during August 2025. Marine Heatwave (MHW) conditions, defined as five or more consecutive days with SSTs above the climatological 90th percentile, also persist over these areas. In contrast, ocean temperatures have cooled off slightly compared to July off the east coast of the North Island. Looking ahead, above-average SSTs are expected to continue around New Zealand through spring (September - November 2025), although the strength of these anomalies may ease somewhat.

The Wholesale Gas Market

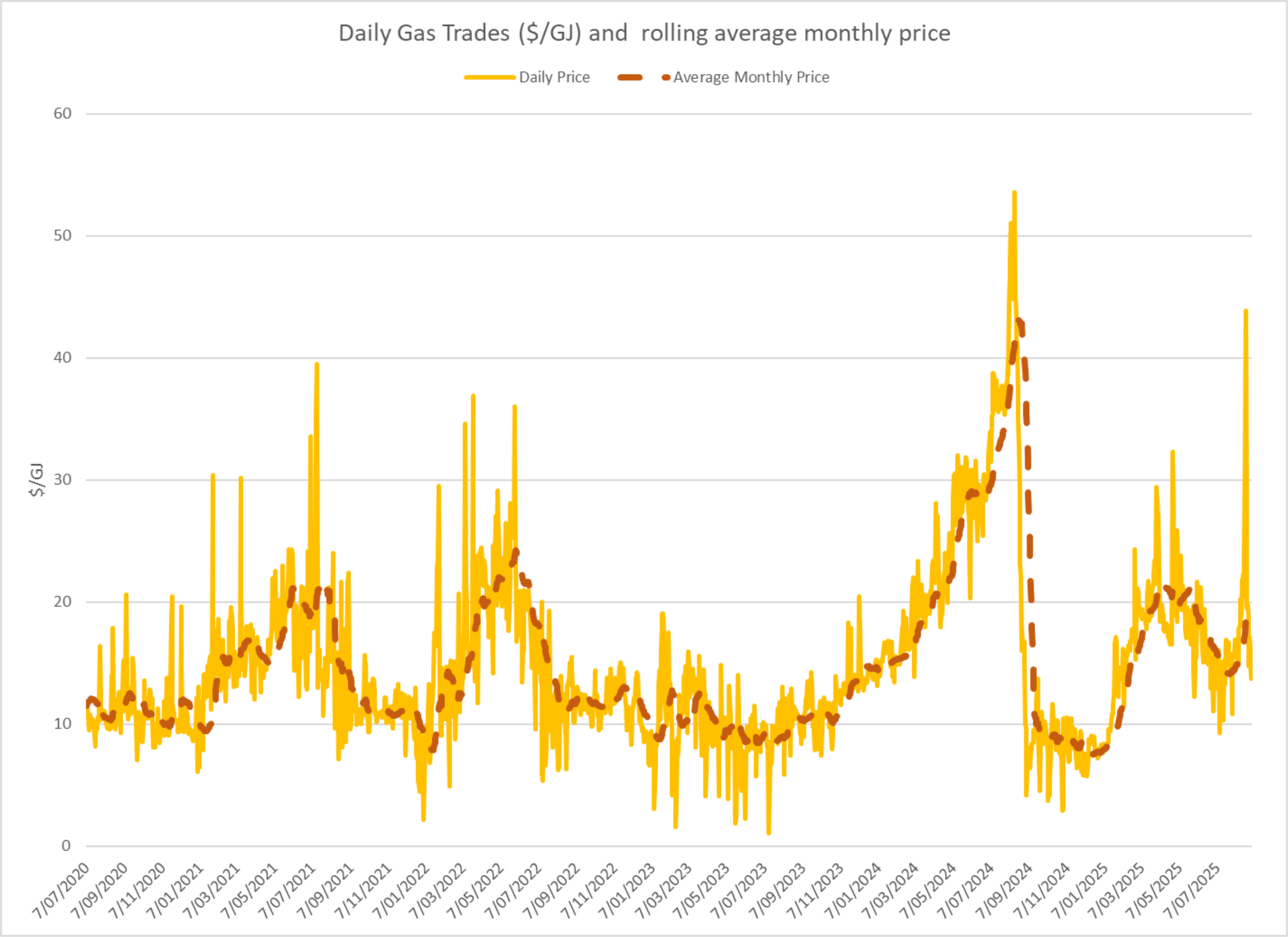

Spot gas prices in August increased significantly. Prices for the month averaged $19.7/GJ – a 39% increase compared to July. Average prices were 50% below what they were at the same time last year. Note that spot gas prices include the cost of carbon (currently around $3/GJ)

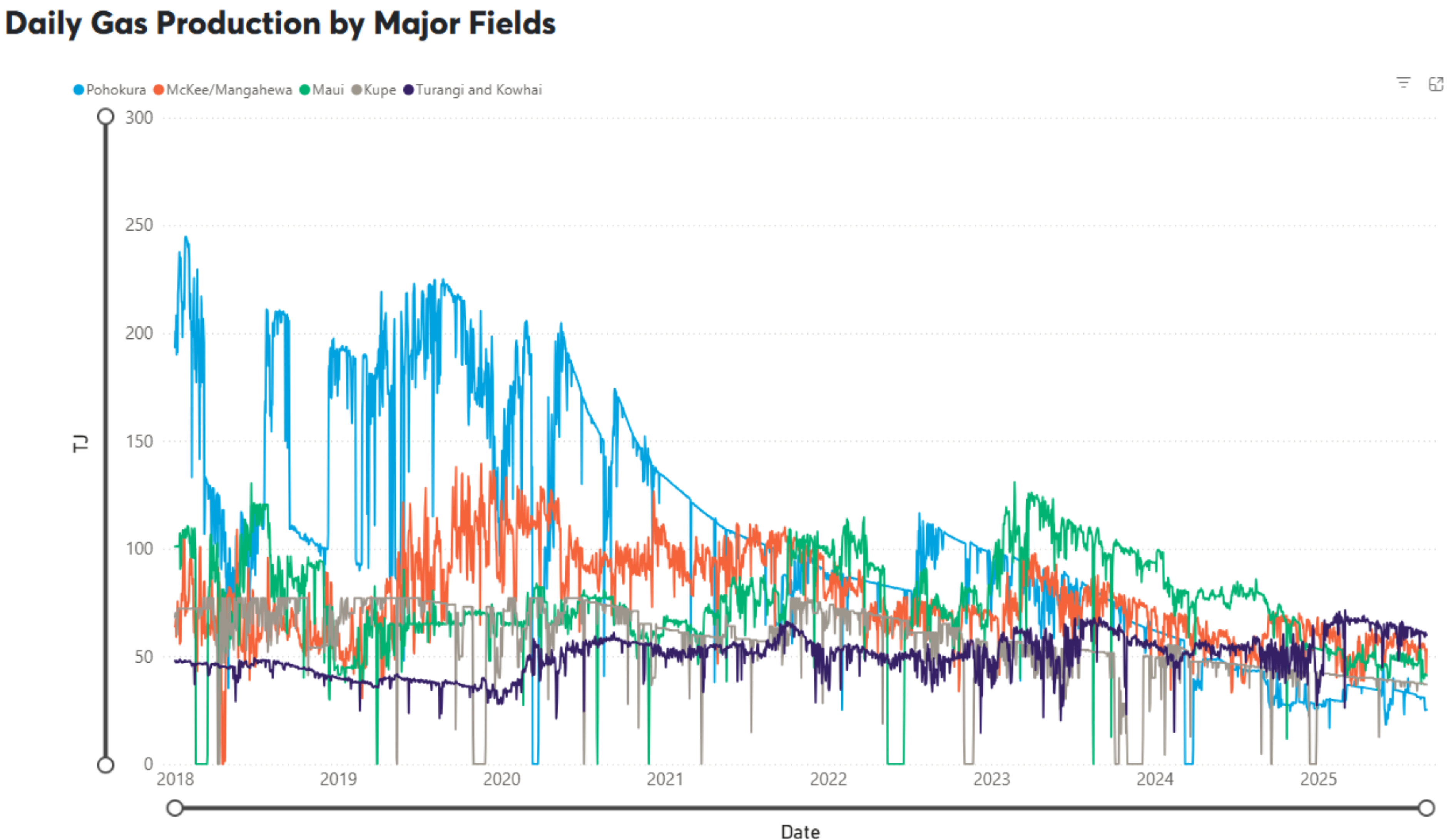

On the supply side most producers reduced output slightly through August. Maui decreased slightly from mid 40s at the start of the month down to the low 40TJ/day by the end. Similarly Pohokura started the month at around 33TJ reducing to the high 20s by the end of the month. McKee / Mangahewa was reasonably consistent through the month averaging 53.5TJ/day. Turangi and Kowhai was again consistently in the low 60sTJ/day.

The following graph shows production levels from major fields over the last 7 years.

Having restarted in July, Methanex reduced gas usage through August from 60TJ/day at the start of the month down to less than 50TJ/day by the end. Huntly maintained usage from last month at 53TJ/day. TCC started up towards the end of August using over 40TJ/day in the last week of the month. Balance Agi-Nutrients (not shown in our data but uses about 20TJ/day) announced in August that it will close its Kapuni urea plant at the end of September for 4 months if it can’t secure a gas supply. Longer-term, a full closure of the plant is possible if an affordable and secure supply of gas can't be found.

The following graph shows trends in the major gas users over the last 7 years.

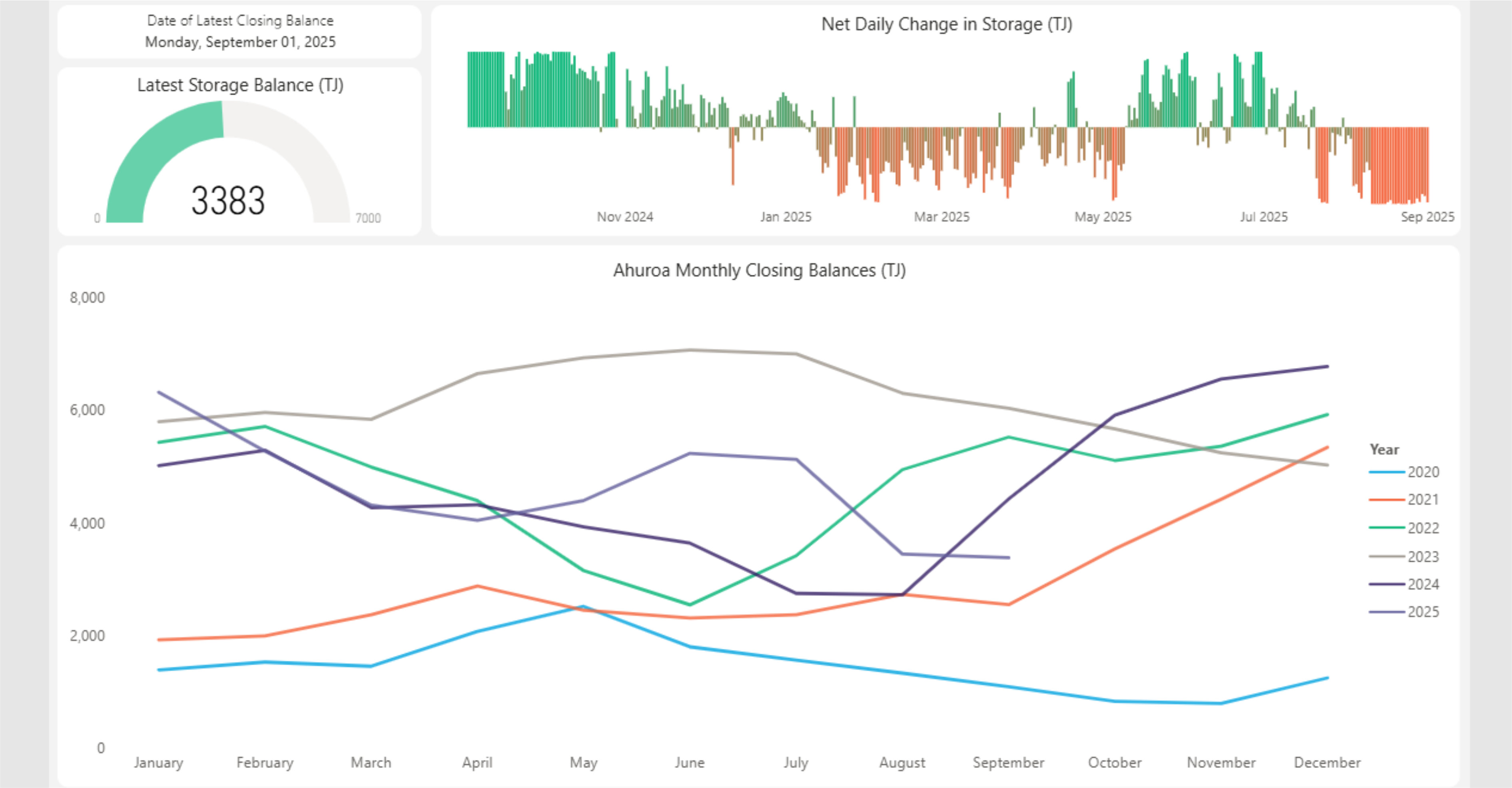

Gas storage is becoming increasingly important as falling production coincides with more variable demand particularly from gas fired electricity generation. The following chart shows how storage at Ahuroa decreased significantly through August. It is now close to average levels seen at this time of year over the last few years.

Internationally, LNG netback prices ended the month at $15.64/GJ – down 9% from last month. Forecast prices for 2025 were down 2% at $17.06/GJ. Forward prices for 2026 were also down 9% at $14.75/GJ. (Note that netback prices are indicative of international prices – they are produced by the ACCC and quoted in Australian dollars. They are net of the estimated costs to convert from pipeline gas in Australia to LNG, hence the term “netback”)

New Zealand does not (yet) have an LNG export/import market, so our domestic prices are not directly linked to global prices. With recent gas supply issues, the Government is now talking about the possibility of facilitating the building of an LNG import facility.

LPG is an important fuel for many large energy users, particularly in areas where reticulated natural gas is not available. The contract price of LPG is typically set by international benchmarks such as the Saudi Aramco LPG – normally quoted in US$ per metric tonne.

The following graph shows the Saudi Aramco LPG pricing for the last 4.5 years as well as forecast pricing for the year ahead. Futures pricing were down over the last month and remain trending down through 2026.

The other main contributing factor to LPG prices in New Zealand is the exchange rate against the USD. The exchange rate hovered around 0.59 for much of August. This remains near the lowest levels seen in recent years. This would tend to push up LPG prices when quoted in NZD.

The Coal Market

The global energy crisis has been as much about coal as it has gas. The war in the Ukraine has driven energy prices, including coal, up. Prices in August decreased ending the month at US$110/T – a 4% fall over the month. These prices are finally returning to levels close to what we expect to see as shown in the following graph of prices over the last 10 years.

Like gas, the price of coal can flow through and have an impact on the electricity market. In July Genesis reported that it purchased about 186,000 tonnes of coal in the June quarter. The company says it currently holds about 699,000 tonnes at Huntly, up from 474,000 at the end of March and 231,000 a year earlier. Genesis says that 500,000 tonnes is the equivalent of about 1,000GWh of electricity storage or 22% of maximum hydro storage in NZ.

Carbon Pricing

NZ has had an Emissions Trading Scheme (ETS) in place since 2008. It has been subsequently reviewed by several governments and is now an “uncapped” price scheme closely linked to international schemes. However, there are “upper and lower guard-rails” set up to prevent wild swings in carbon price that act as minimum and maximum prices. These increased in December 2023 to $173 and $64 respectively. Carbon prices increased 1% in August to $58.

As the carbon price rises, the cost of coal, gas or other fossil fuels used in process heat applications will naturally also rise. Electricity prices are also affected by a rising carbon price. Electricity prices are set by the marginal producing unit – in NZ this is currently typically coal or gas or hydro generators, with the latter valuing the cost of its water against the former. An increase in carbon price can lead to an increase in electricity prices in the short to medium term (as the marginal units set the price). A carbon price of $50/t is estimated to currently add about $25/MWh (or ~2.5c/kWh) to electricity prices. In the long term the impact should reduce as money is invested in more low-cost renewables and there is less reliance on gas and coal fired generation.

EU Carbon units increased in August to 74.3 Euro/tonne – up 4%. Australian Carbon Units also increased 4% to AUD$37.15

About this Report:

This energy market summary report provides information on wholesale price trends within the NZ Electricity Market. Please note that all electricity prices are presented as a $ per MWh price and all carbon prices as a $ per unit price. All spot prices are published by the Electricity Authority. Futures contract prices are sourced from ASX.

Further information can be found at the locations noted below.

- Transpower publishes a range of detailed information, which can be found here: https://www.transpower.co.nz/power-system-live-data

- The Electricity Authority publishes a range of detailed information, which can be found here: https://www.emi.ea.govt.nz/

- Weather and Climate data – The MetService publishes a range of weather-related information, which can be found here: https://www.metservice.com/

Disclaimer: This document has been prepared for informational and explanatory purposes only and is not intended to be relied upon by any person. This document does not form part of any existing or future contract or agreement between us. We make no representation, assurance, or guarantee as to the accuracy of the information provided. To the maximum extent permitted by law, none of Smart Power Ltd, its related companies, directors, employees or agents accepts any liability for any loss arising from the use of this document or its contents or otherwise arising out of or in connection with it. You must not provide this document or any information contained in it to any third party without our prior consent.

About Smart Power:

Smart Power is a full-service Energy Management consultancy. Apart from Energy Procurement, Smart Power can also provide:

- Technical advice on how to reduce your energy use & emissions

- Sustainability Reporting

- Invoice Management Services

We also offer boutique energy and water billing services for landlords/property developers.

Contact us here or call one of our offices to talk to our experienced staff about how we can assist you with achieving your energy goals.

© Copyright, 2025. Smart Power Ltd